SOLIDERE's License Expires in 2029. Renewal or Liquidation?

Lebanon’s government should use the opportunity to modify and balance the real-estate company’s mandate, with the aim of extracting public value from the heart of its capital city and spill them over to the rest of the urban agglomeration. In this note, the Beirut Urban Lab outlines key facts concerning SOLIDERE and proposes three sets of directions for Lebanon’s government to consider.

Brief History

When SOLIDERE was established in 1994 based on a revised legal framework for “real-estate companies,” Lebanon was emerging from 15 years of civil war (1975-1990). At the time, special facilities were extended to the company that took hold of 4.03 million square meters of built-up area, liquifying all property in the forms of shares in a joint-stock company (Shares A).1 Property claimants who rejected the share were left with the only choice of buying back their claimed properties with restrictive measures. In addition, investors were invited to acquire shares (Shares B) that would inject capital in the company and allow its operation.2 This constituted a first extension of the existing real-estate company scheme within Lebanon’s regulations, one of many facilities that would eventually be granted to the company.

The forceful takeover of property was justified as the only way to muster the coordination capacity needed to launch Beirut's reconstruction3: A real estate holding company would be empowered to assemble fragmented property, sort multiple inheritances, resolve conflicting property claims, address heritage issues, and turn a war-shattered historical core into a global hub of tourism and services.4 The arrangement was packaged with promises of jobs, prosperity, and wealth within a framework of so-called trickledown economics.5

A detailed master plan6 was developed and SOLIDERE was allowed to separate the built-up ratio from land, allowing for a Transfer of Development Rights7 that is not permissible elsewhere in the city. SOLIDERE also adopted high-end and detailed guidelines for repair, and it mandated that clients who buy back/acquire existing buildings adopt the same detailed standards. This led to the development of uniquely high standards for building and public space design but also rendered property reclamation particularly difficult and constrained the ability to intervene in Beirut Downtown to the most well-off developers.8

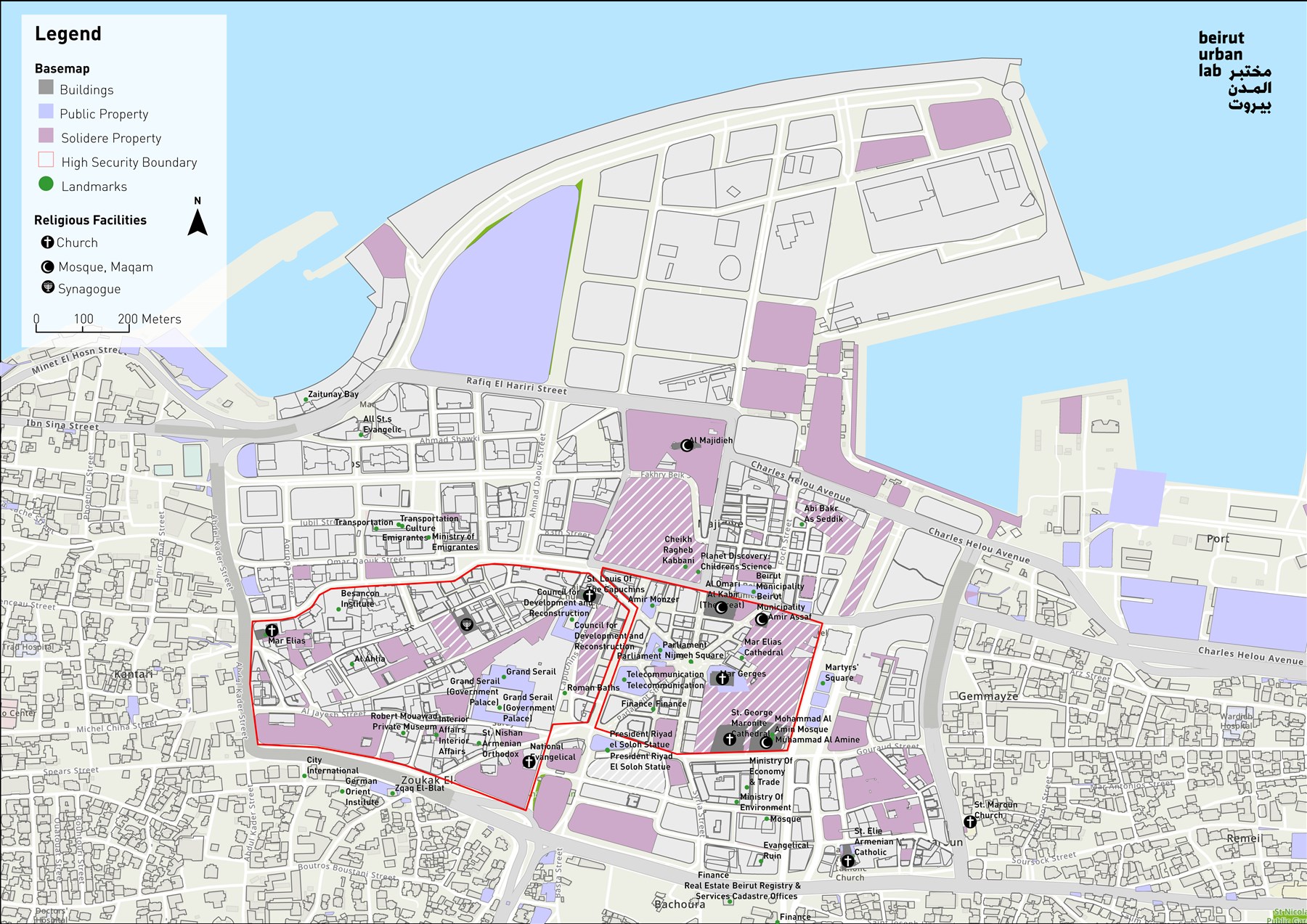

In the original scheme, SOLIDERE was mandated to plan, develop, and sell all properties, distribute profits to shareholders, and get liquidated by 2019,9 handing back its prerogatives to the Municipality of Beirut and relevant public authorities. Three decades later, the bargain looks lopsided. Although a well-designed urban fabric has materialized in a handful of carefully planned and greened—albeit highly exclusive—neighborhoods, the original case for SOLIDERE's market power — coordinating reconstruction amid chaos, has largely run its course. What remains is a company sitting on roughly 1.35 million square meters of land bank10 (down from over 4 million), still holding undeveloped parcels in the Biel area and in Martyrs' Square, and still pricing its own future privately, while waiting for the market, rather than the public, to decide when development resumes (see map 1 below).

Exceptions and Benefits

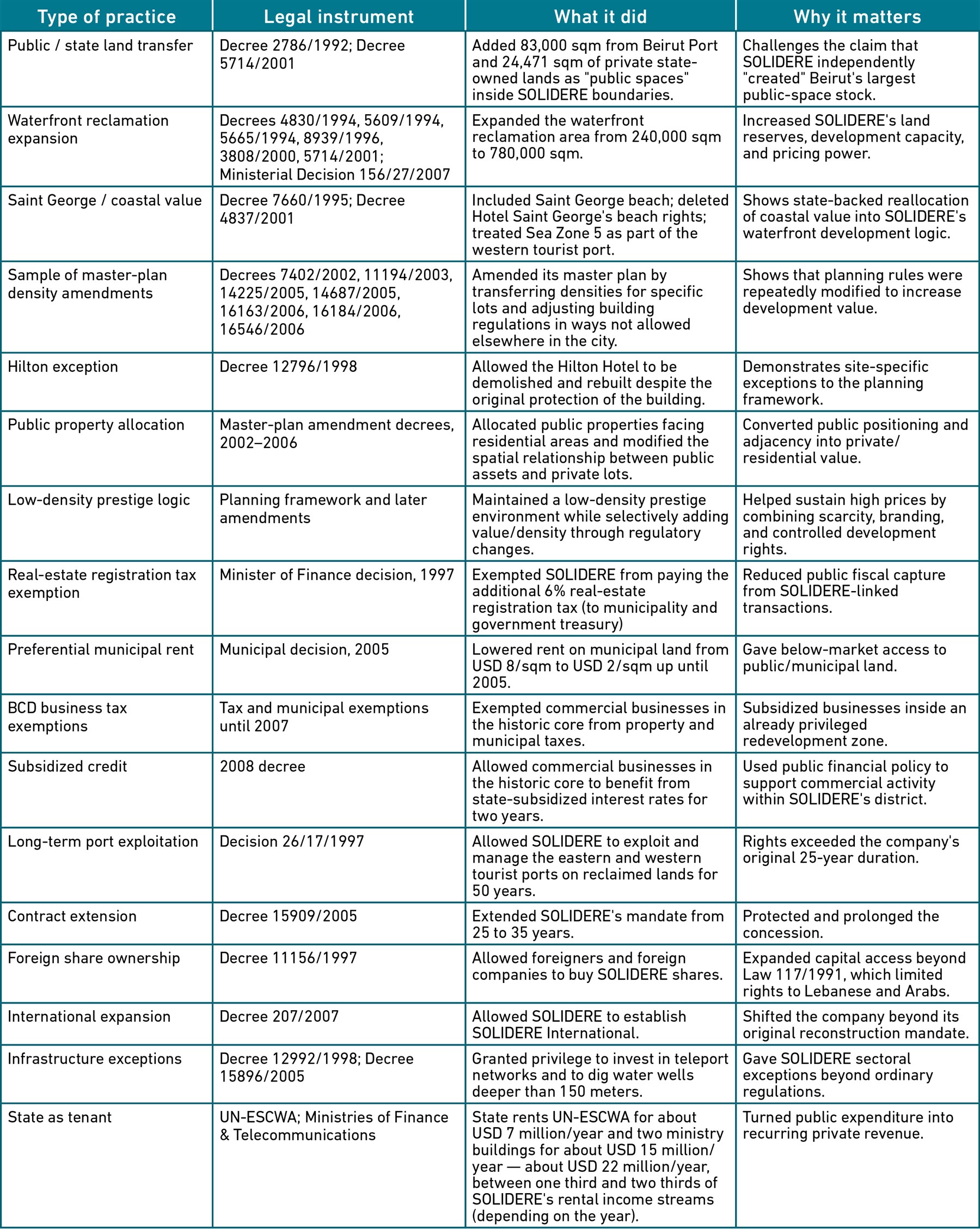

Since 1994, and beyond the original facilities that accompanied its establishment, SOLIDERE has benefited from substantial public subsidies and privileges, estimated around US$3 billion. These include waterfront land reclamation rights worth US$2 billion,11 tax exemptions worth roughly US$590 million,12 and direct state land transfers (see Table 1 for a longer list). In return, SOLIDERE distributed US$1.2 billion in dividends13 and rebuilt infrastructure with a total cost of one billion dollars—although to-date, its value was captured by SOLIDERE rather than the public,14 as well as sections of the city center—nonetheless leaving major public obligations unfulfilled (e.g., green areas including the seafront park and the Garden for Forgiveness, a Museum, and Martyr Square’s parking garage15).

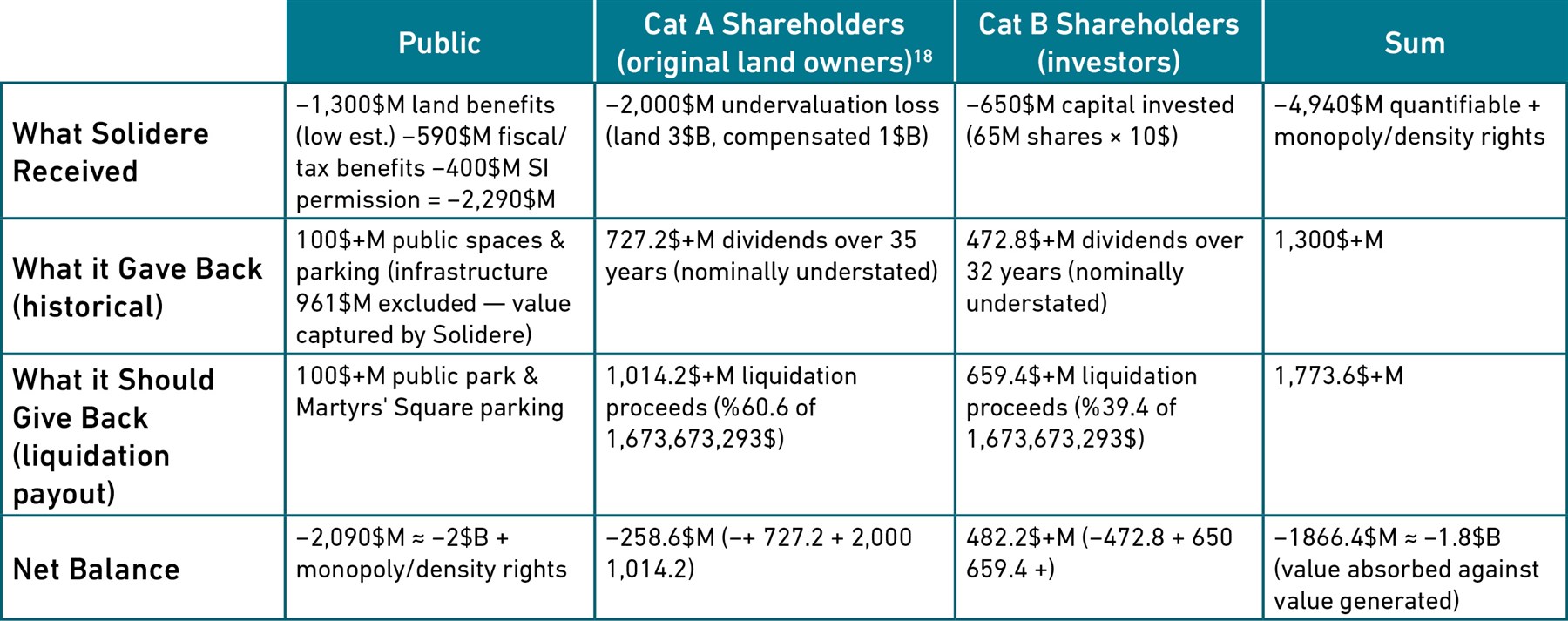

In addition, since its creation, SOLIDERE has also sold 2.66 million square meters of land and air rights for US$4 billion.16 The company currently values its remaining 1.35 million square meters at US$2.5 billion—a valuation gap consistent with a 2012 claim that its land bank was worth US$8billion.17 The gap between the actual profit reaped from pre-2012 sales and the estimated land values is indicative of the company’s business strategy: SOLIDERE is not pricing development, it is pricing patience. The company is waiting for political and market sentiment to turn before selling the remaining land stock—while the public bares the cost of an inactive city center. This strategy is built within the project’s design: While a private real estate company is accountable to maximize the profits of its shareholders, a public agency would be accountable to the urban collectivity it serves.

Liquidation payout is estimated at accounting figures (SOLIDERE’s 2023 Balance Sheet19 assumes 1.6 billion USD in Shareholder equity, it is assumed SOLIDERE will be liquidated at this value, not the projected value of its real estate in 2023 report of the Board of Directors, which is placed at 4 billion USD and not shared publicly). The balance sheet figures are consistent with SOLIDERE’s current market capitalization.20 The gap between the two valuations represents the value SOLIDERE excepts to extract from the extension. (Source: Ahmad Sabra Thesis, forthcoming)

The Economic Model

SOLIDERE's development model fits squarely within the rentier logic that defined Lebanon's post-civil war economy.21 In this model, real estate was both the dominant sector and the macroeconomic stabilizer that kept the post-war economy afloat.22 Rather than approaching land as a scarce resource needed to support a productive economy, land was reduced to a financial asset to store wealth and turned into a lever deployed to attract foreign capital into the country.23 Consequently, land prices rose well above local means, harming economic productivity and undermining the right to housing. In this context, a venture as large, coordinated, and symbolic as SOLIDERE should be considered as one of the early drivers of this rentier model and the speculative property practice it engendered.

The 2025 Cabinet has announced its intention to shift away from the rentier model and develop productive sectors of the economy that would foster employment and reduce brain drain.24 As such, how Lebanon’s government chooses to approach the renewal of SOLIDERE’s mandate falls at the heart of its credibility. An unconditional renewal would tell Lebanon, and the world, that the country's so-called recovery is still organized around extracting value rather than creating it, and that reform was mostly branding rather than action. Conversely, a studied and conditional approach can send the appropriate signal but also serve as a spark to regenerate a direly needed urban economy for Lebanon’s capital. In what follows, we outline some of the directions that the government should consider.

Recovering Beirut’s Historic Core

Extending SOLIDERE’s mandate unconditionally or in exchange for minor concessions will amount to prolonging an already failed recipe. However, a conditional extension that allows the government to shift the company’s accountability, albeit partially, to the public interest of all city-dwellers may be a desirable compromise in the current conditions. In other terms, if a 2029 renewal is adopted, it should be limited, and it should introduce a reversal in the original development model while preserving the urban-design gains and extending their benefits to the wider city.

Redistributing Profit

Prior to any negotiation, the government should hold SOLIDERE accountable for the commitment it has left unfulfilled: City parks, including the seafront public park (recently named Hariri Park) where no greenery has been planted despite a now 35-year-old commitment, but also execution plans for public parking garages and cultural assets should be pre-requisites to an actual extension of the mandate. The cabinet could consider a 2-year extension to ease the 2029 deadline and allow SOLIDERE to demonstrate its good will prior by initiating actual project execution before determining the duration and conditions of the larger extension that should not exceed 10-15 years.

In addition, SOLIDERE's real current market value—likely around US$1.6 billion25- should be assessed against the company's claim of US$3.5 billion in assets. Consequently, any value (in revenues) created above the US$1.6 billion baseline should accrue to the city, not to shareholders who have already been compensated many times over relative to their original contribution.26 A ceiling set below the US$1.6 billion mark with anything earned above returned to the city or the public treasury removes SOLIDERE's incentive to wait out the market, and makes swift development the more profitable choice for everyone involved.

Three Pathways

Theoretically, Lebanon’s government has three pathways to respond to SOLIDERE’s demand of contract extension. However, in practice, we argue below that only the conditional renewal option is viable.

Outright Liquidation: A strict implementation of the current text indicates that, short of renewal, SOLIDERE should sell its full land bank in a public auction by the deadline of its mandate (2029). This might look like the clean alternative to renewal, and is a solution frequently advocated by Lebanon’s activists. However, upon closer examination, the long-term effects of this option may further compound the negative externalities generated by the company. Indeed, dumping 1.35 million square meters onto a largely stalled, still-recovering property market devaluates land values across the city center and beyond, hence locking-in a fire-sale price for assets the public has spent three decades subsidizing. In current economic circumstances, it is likely that a handful of well-networked investors would acquire and hoard the land bank at devaluated prices, capturing all the value for private interest and reproducing the same concentrated control that defined SOLIDERE's monopoly, without a mechanism in place to capture or redistribute that value for the public.27 Moreover, a sudden dissolution leaves no clear path to actually complete the unfinished public obligations— i.e., the seafront park, the parking garages—or to bind whoever inherits the parcels to deliver those. Liquidation trades the patient extraction of public value for the appearance of decisiveness and ignores Lebanon's limited institutional capacity which prevents it from managing well the handover.

Controlled Fragmentation: By splitting SOLIDERE into two or three companies, it is possible to see the city’s core regenerated through a healthy market-based competition as part of an economic-development vision, with affordable commercial space, public open space along the waterfront, and the mixed-use development that creates jobs rather than just luxury units for absentee buyers. There are many advantages to this option, most notably the creation of healthy competition, the injection of new capital, and allowing for opportunities to swiftly redistribute company assets. However, fragmentation only works if clear and powerful institutional oversight prevents collusion among stakeholders. It also requires solid central and urban governance frameworks that secure accountability and adequate urban standards. In short, while likely the most desirable, this option requires an institutional oversight that is arduous to uphold by public institutions at the current moment.

Conditional Renewal: A negotiated continuation of the SOLIDERE mandate provides the pathway to recover at least some real public value, while keeping the company in place for an additional 10-15 years and building its assets. As noted above, such negotiation should start from the premise of a ceiling over profit and the necessity to balance the mandate towards stakeholders with benefit for city dwellers. At least two (not necessarily exclusive) orientations can be concomitantly considered:

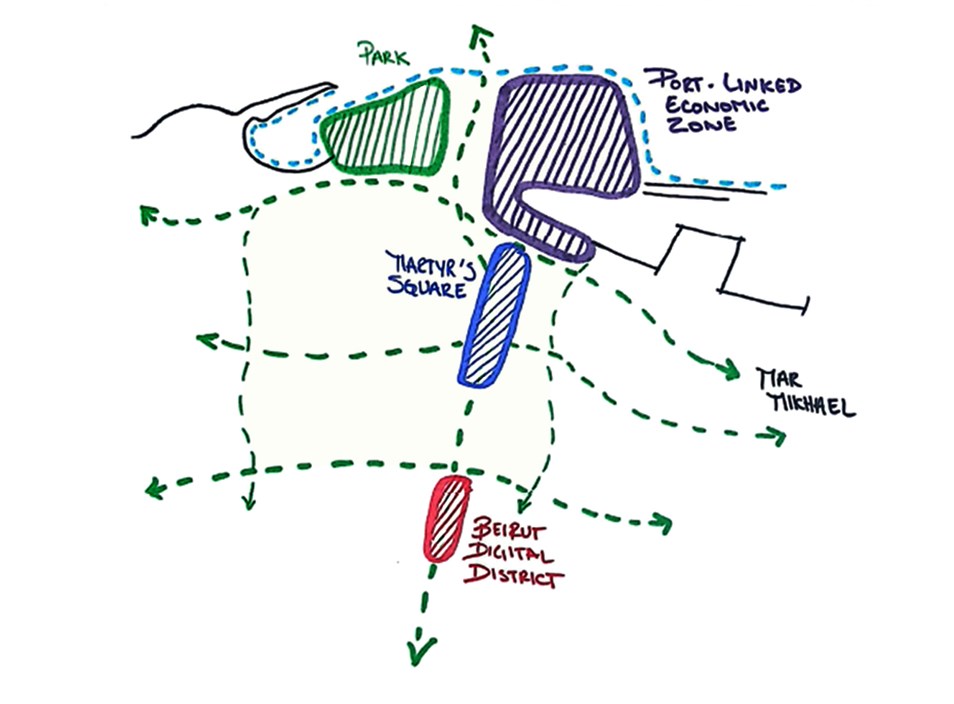

- Transform the economic model that guides SOLIDERE’s urban form to allow for much larger public concessions: By revising the master plan and introducing enforceable timelines to activate idle land rather than open-ended discretion, the government can set the first step to reap public benefits from private development. By way of example, a revised master plan should reconsider, first, the weight of the projected traffic imposed on the city, once planned developments are implemented, and it should therefore reduce densities and vehicular mobility particularly at the level of the waterfront. A revised masterplan would further mend urban ruptures by restitching the historic core’s neighborhoods with surrounding city quarters and extending existing functions into the historic core (e.g., an extension of the Beirut Digital District land uses toward Martyrs' Square; mixed income housing in all residential zones; co-working spaces). Finally, planners could reconsider the connection to the port redevelopment, hence restitching the city’s waterfront and linking through the proposed port interventions towards Mar Mikhael.28 Further details should be introduced once the principles of integrated and balanced development are adopted.

- Impose a disciplined enforceable timeline of 10-15 years for land sales and development and a hefty value capture mechanism from land sales to be reinvested in the wider city: Public authorities should secure a percentage of the profits gained from SOLIDERE’s land sales and earmark them to implement existing plans that would benefit the entire city, supporting a project of national interest such as public mobility and/or other targeted interventions such as long-term visions designed to ease urban shared mobility and improve urban walkability across Beirut.29 This approach would follow the model of land value capture implemented in other cities, where well-identified public authorities are able to reap profits from land value increases to reinvest them in concrete projects earmarked for the public good.30

Given that the valuation of properties within SOLIDERE's jurisdiction is subject to the same uncertainties documented across the rest of the city,31 owing to the absence of transparent valuation models and a highly speculative land market, the Beirut Urban Lab insists that a "value capture" mechanism that earmarks a percentage of gains to go back to public coffers and be reinvested in developmental intervention rather than just a ceiling on profit, is highly desirable, next to a tax on vacancy32 to disincentivize speculation, and a gradual schedule of property transfer.

Both options discussed above are feasible, and Lebanon’s government should negotiate a blended outcome that merges them, while introducing binding deadlines to liquidate property and measures to fight vacancy.

Short of such concessions, the government should retain the option of rejecting SOLIDERE’s renewal as viable. It may consider transferring property management to a newly created public-private or a partnership with a nonprofit such as a university that would introduce direly needed economic activities to the historic core. Alternatively, the government could also consider other options within Lebanon’s planning regulations, such as the establishment of a public agency with temporary jurisdiction over the area. These options may seem risky, and BUL encourages serious consideration of a conditional and limited extension, but they remain more desirable than the prolongation of the current modus-operandi or a renewal with the mere concession of one or two buildings that leaves the same development model unscathed.

In Conclusion

Lebanon’s government has an opportunity to reverse the tides and elaborate a concrete strategy that materializes its claims of a new economic model. To be clear, none of this is about punishing SOLIDERE for the act of rebuilding Beirut's center —that work mattered, and the urban-design gains exist. Neither is it possible to bring justice to the thousands of city dwellers who lost property with the establishment of SOLIDERE. However, recognizing that the original mandate has been fulfilled, that the company's main remaining strategy is to hold the city’s historic core and wait, and that the public has already paid enough: in subsidies, in land, in a decade-long extension already granted, our argument is for setting Beirut and Lebanon on a new path.

Renewing SOLIDERE's license as it stands lets the emblem of Lebanon's pre-2019 rentier economy write the next chapter in the already war-torn country. Lebanon should choose differently: conditional renewal with teeth, or controlled fragmentation with a plan. Either way, Downtown Beirut should finally become a productive and lived city center, rather than a land bank waiting for better days, or a playground for the rich and affluent.

Endnotes

1 For more on the legal structure of SOLIDERE, check: Mahmassani, M. S. (1998) “The Legal Framework for Reconstruction by the Private Sector of Post-Conflict Beirut Central District”, ICSID Review – Foreign Investment Law Journal, 13(2), 455–477.

2 It is widely conceded that SOLIDERE benefitted from undervaluing land values at the time, whereby original landowners were compensated with so-called Category-A shares estimated at US$1 billion, a value that the Association of Aggrieved Property Claimants placed at US$3 billion. Consequently, original property holders estimate that they have collectively incurred a 2 billion USD loss with SOLIDERE’s inception. For more, on the inception of SOLIDERE, check: Makdisi, S. (1997) “Laying claim to Beirut”, Critical Inquiry, 23(2), 660–705.

3 For contrasting interpretations of the reconstruction of Beirut's city center, see Hourani, N. (2012). “From national utopia to elite enclave: "Economic realities" and resistance in the reconstruction of Beirut”, in: Global Downtowns, M. Peterson & G. W. McDonogh (eds.), University of Pennsylvania Press, pp. 136–160 and Nasr, J. & Verdeil, E. (2008), “The Reconstructions of Beirut”, in The City in the Islamic World, Makdisi, S, Raymond, A. and Rabbat, A. (eds.), London:Brill, pp. 1111–1144. Both authors critically examine the official rationale underpinning the reconstruction process. Saliba, R. (2004) offers a more supportive assessment of the SOLIDERE-led reconstruction strategy in Beirut City Center Recovery: The Foch-Allenby and Etoile Conservation Area, Academy Editions.

4 Makdisi (op-cit), Leenders (2003), and Hourani (op-cit) document the divergence between the stated objectives of Beirut's postwar reconstruction and its outcomes. Makdisi analyzes the discourse of prosperity and national renewal that underpinned the reconstruction project, Hourani further examines how the reconstruction evolved from a national project into an elite-centered urban development model, and Leenders emphasizes its political economy, showing how elite networks and governance arrangements concentrated benefits rather than delivering broadly shared gains.(See: Leenders, R. (2003) “Nobody having too much to answer for: Laissez-faire, networks, and postwar reconstruction in Lebanon”, In S. Networks of Privilege in the Middle East, Heydemann (ed.), Palgrave Macmillan, pp. 169–200.

5 Mango, T. (2014). The Impact of Real Estate Construction and Holding Companies: A Case Study of Beirut's SOLIDERE and Amman's Abdali [Doctoral dissertation, University of Exeter]. Open Research Exeter. https://ore.exeter.ac.uk/repository/handle/10871/17497

6 The detailed master plan is a planning tool within Lebanon’s regulations that specifies building regulations at the scale of the lot. For more, see SOLIDERE’s Description of the masterplan at: https://www.SOLIDERE.com/city-center/urban-overview/master-plan and Stewart, D. J. (1996) “Economic Recovery and Reconstruction in Postwar Beirut”, Geographical Review 86(4), 497. https://doi-org.ezproxy.aub.edu.lb/10.2307/215929

7 Transfer of development rights is a zoning and urban planning tool that allows the separation of the right to build on a property from the land itself. For more, see Lane, R. (1998) “Transfer of Development Rights for Balanced Development”, Lincoln Institute of Land Policy, at: https://www.lincolninst.edu/publications/articles/transfer-development-rights-balanced-development/ last visited on July 1, 2026.

8 Check Makdisi, S. (1997, op-cit) and Marot, B. (2018). Developing Post-War Beirut (1990–2016): The Political Economy of Pegged Urbanization. McGill University, School of Urban Planning.

9 Check SOLIDERE’s Articles of Incoporation, Chapter Ten: “Dissolution of the Company, Liquidation and Litigation”. Link: https://www.SOLIDERE.com/sites/default/files/attached/.pdf?__cf_chl_f_tk=fhgN5cL.XTNlOBwu4Q_17O.c2LhnP4xgE5zpdkPrKVg-1782851554-1.0.1.1-Q_JQTpTp0On3Jfv9AADnI6Et8A.YuEmW90dtU9Ne1kk

10 Source: SOLIDERE Board of Directors Report 2023.

11 SOLIDERE was given ownership over reclaimed area with a total surface gain of 730,000sqm, up from the initial 270,000sqm. The latter were valued at US$700 million (Assafir daily, issue 6856, 15/08/1994) Link: https://archive.assafir.com/ssr/737055.html last visited on July 2, 2026.

12 SOLIDERE is exempt from corporate taxes (17% of net income (US$1.4 billion) yields 230 million), and From land registration taxes upon sale ( 6% of 4 billion in sales (240 million). See more: https://taxsummaries.pwc.com/lebanon/corporate/taxes-on-corporate-income

13 For SOLIDERE dividends, see: https://www.SOLIDERE.com/corporate/investor-relations/dividends, last visited July 2, 2026.

14 SOLIDERE 2023 Balance Sheet , Available on SOLIDERE website at: https://www.SOLIDERE.com/sites/default/files/attached/2023_balance_sheet.pdf, last visited July 2, 2026.

As both infrastructure builder and near-monopoly landowner of the district it serviced (Law 117/1991), SOLIDERE captured the land-value uplift its works created — self-investment rather than public benefaction — and was separately compensated with 291,800 square meters (later made 780,000 sqm) of reclaimed waterfront land under its 1994 CDR agreement. See SOLIDERE, Articles of Incorporation; SOLIDERE, Annual Report 2006; Makdisi, "Laying Claim to Beirut," Critical Inquiry 23, no. 3 (1997): 661–705.

15 Source: SOLIDERE Board of Directors Report 2023. We note that there have been disagreements over who finances the construction of the parking, but the responsibility to see it happens fell unequivocally on SOLIDERE.

16 SOLIDERE financial data drawn from the following sources: for 1994–2000, SOLIDERE, Excerpts for Analysts, July 2012, available at SOLIDERE.com; for 2001–2025, SOLIDERE Annual Financials Reports (2016, 2018, 2019, 2021, 2022, 2023) and Quarterly Financials Reports (Q2 2017, Q2 2019, Q2 2020, Q2 2021), published by the Lebanese Company for the Development and Reconstruction of Beirut Central District (SOLIDERE), Beirut.

17 SOLIDERE Annual Report 2012 : https://www.SOLIDERE.com/sites/default/files/attached/ar2012.pdf, last visited July 2, 2026.

18 It should be noted that this accounting treats Category A as a single undifferentiated class across the full thirty-five-year period, a simplification adopted for tractability: It assumes original landowners held their shares for the entire 35-year period. In practice many original owners sold their shares during periods of acute liquidity need long before the gains captured here were realized (Hourani 2012, cited above), meaning the loss borne by the actual original landholders is almost certainly larger than this table shows, and the dividends counted here increasingly accrued to subsequent buyers rather than to the people the compensation was nominally designed to make whole.

19 Available on SOLIDERE website through: https://www.SOLIDERE.com/sites/default/files/attached/2023_balance_sheet.pdf, last visited July 2, 2026.

20 Market capitalization — the total value of a company's shares on the stock market — is calculated by multiplying the number of shares by their current share price. SOLIDERE's nominal market capitalization stands at approximately US$12 billion, but this figure is denominated in "lollars": US dollars trapped in the Lebanese financial system since the 2019 financial collapse, which trade at roughly 12–15% of their real dollar value. Adjusted for this discount, SOLIDERE's true market capitalization is closer to US$1.4–1.8 billion. Check http://www.bse.com.lb/Market/Quotes/tabid/89/Default.aspx for more, last visited July 2, 2026.

21 For more, see Bisat, A., & Diwan, I. (2024, June), Towards a Productive "New" Lebanon, Issam Fares Institute for Public Policy and International Affairs. Link: https://www.aub.edu.lb/ifi/Documents/Towards-productive-New-Lebanon.pdf, last visited July 2, 2026.

22 Marot B (2018) “Growth Politics from the Top Down: The social construction of the property market in post-war Beirut”, City 22(3): 324–340.

23 Fawaz, M., Zaatari, A. and Mneimneh, S. (2026). The Ripples of Housing Financialization: Old actors, new practices in Beirut (Lebanon). Environment and Planning A. Online first. https://doi.org/10.1177/0308518X26145208

24 Ministerial Statement of the government of Prime Minister Nawaf Salam ("Reform and Rescue"), adopted by the Council of Ministers at Baabda Palace, 17 February 2025 (parliamentary confidence vote, 26 February 2025). Draft text: An-Nahar, 17 February 2025, annahar.com/Lebanon/Politics/195756; English version: Dearborn.org, 25 February 2025, dearborn.org/en/preview/full-text-of-the-ministerial-statement-of-prime-minister-nawaf-salams-government-65569; official Arabic text at pcm.gov.lb.

25 SOLIDERE 2023 balance sheet: https://www.SOLIDERE.com/sites/default/files/attached/2023_balance_sheet.pdf and Market Capitalization (explained above).

26 This, at least, is the case of those who acquired “Share B” by investing in the company, or who bought “Share A” later from the original owners.

27 Fawaz, M., & Zaatari, A. (2024). Housing Vacancy in Beirut 2023: Drivers and Trends. Policy Report, Beirut Urban Lab, American University of Beirut, June 2024. Link: https://beiruturbanlab.com/en/Details/1983

28 By way of example, see earlier theses produced by students at the MUPP and MUD programs in the Maroun Semaan Faculty of Engineering and Architecture and the American University of Beirut such as Sarieddine, M. 2020. An Alternative to the Market Driven Urban Development, the Case of the Normandy Landfill and Darwish, I. 2020. Mitigating the gentrification impacts of innovation districts : the case of Beirut Digital District (BDD) and Bachoura, Beirut.

29 For a good example, see Beirut’s soft mobility plan (the Plan de Deplacement Doux), Municipalité de Beyrouth & Région Île-de-France. (2013). Reconquérir les espaces publics de Beyrouth : Vers une politique d'aménagement durable. Bureau de la Région Île-de-France au Liban. Link: https://citesunies.s3.amazonaws.com/pages/5f4f995992fc3.pdf; last visited July 2, 2026.

30 Lincoln Institute Staff. (2018, October 16). Value capture: This year's big idea: Unlocking the value of land. Land Lines, Lincoln Institute of Land Policy. https://www.lincolninst.edu/publications/articles/value-capture/

Beirut Urban Lab. (2023, March 15–17). City Debates 2023: Taming the growth machine — the promises and pitfalls of land value capture [Conference]. Department of Architecture and Design, American University of Beirut. https://beiruturbanlab.com/en/Details/1902/city-debates-2023-taming-the-growth-machine,-the-promises-and-pitfalls-of-land-value-capture

31 Fawaz, M. and Zaatari, A. (2025). Valuations or Speculations? Challenges and Recommendations for Property Valuation in Lebanon, at: https://beiruturbanlab.com/en/Details/2034 last visited on July 6, 2026.

32 Fawaz, M. and Zaatari, A. (2024) Housing Vacancy in Beirut: Drivers and Trends, at: https://beiruturbanlab.com/en/Details/1983, last visited on July 6, 2026.